Don't Crowd-Fund Health Care; Vote For It (by Tasha Nelson)

I’m conservative on some things and less on others. A true swing voter, a moderate. A Republican was as likely to get my vote as a Democrat —dependent on their voting history on issues important to me. Historically, I leaned more Republican than Democrat until last year, when the Affordable Care Act (ACA) came under fire and I became terrified that my son might lose the health care vital to his survival.

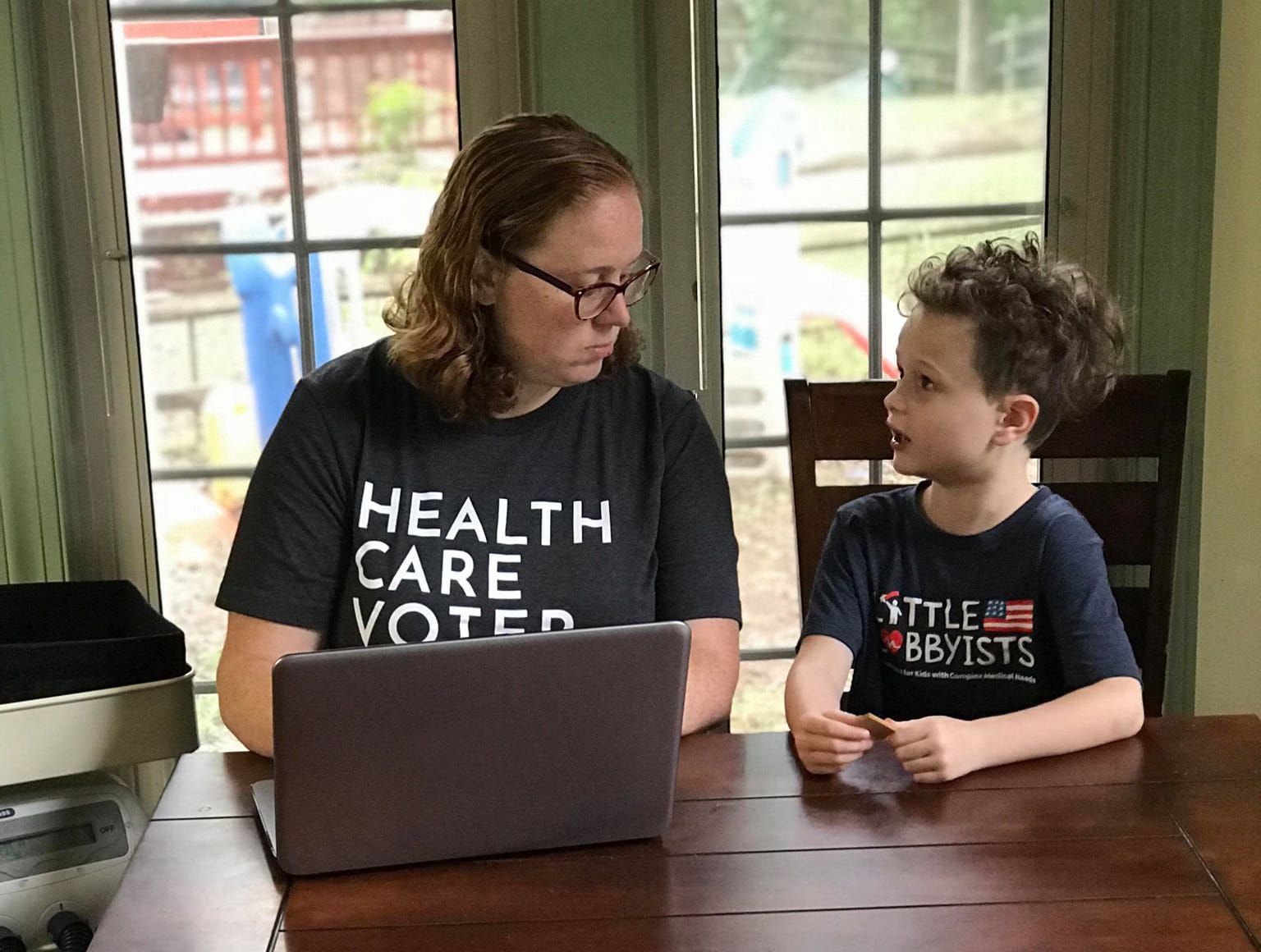

My son Jack is 7 and has a fatal genetic disease called Cystic Fibrosis. This disease is scary, profoundly expensive (just one of the 14 medications he needs to survive is $1,200 per month), excluded from life insurance policies, and fatal.

When Jack was born the full protection for pre-existing conditions provided by the ACA wasn’t yet in place. When he contracted MRSA (a very scary infection), I used up all my vacation time and FMLA to care for him and faced losing a job I’d held for 10 years, knowing my son’s disease made him largely uninsurable. I was terrified that if I lost my job, I’d also lose my son.

Fortunately, I was lucky. The CEO of the huge company I worked for had a heart. He learned of my dilemma and allowed me to work from home. What a relief that was! For 3 months I worked from home, feeling more secure, but still terrified. I’d experienced exactly how quickly my son could go from having all he needs – to having nothing at all. It wasn’t until the full protection of the ACA took effect in January of 2014 that I felt safe. For the first time since Jack was born insurance companies couldn’t discriminate against him by withholding coverage.

Others weren’t as lucky as I was. Their CEO didn’t save their job, their child was born, and died, before the ACA. In the history of health insurance in this country those of us with pre-existing conditions have only experienced 4 years of guaranteed coverage, and we’re already standing on the edge of losing it.

I am a mom fighting for her son’s right to live his healthiest life.

I speak from experience. I’m not a person raging from behind the safety of a keyboard, I’m not a person whose feelings are hurt easily, and I don’t make assumptions. I do speak in person with my politicians at every opportunity, and I actively seek those opportunities out. I educate myself before making any political decision (or post).

No candidate who voted yes on the Tax Bill that weakened that ACA or in favor of short-term “junk” insurance will get my vote. I am a #HealthCareVoter, my son Jack is a #LittleLobbyists, and Jennifer Wexton will get my vote over Representative Barbara Comstock, because Comstock has proven to me that she won’t protect us and she failed my son with her votes.

Many Republicans I’ve spoken with have argued that the Tillis Bill is the GOP’s answer to protecting pre-existing conditions. This is a half truth, at best. While the bill does prevent insurance companies from excluding people with pre-existing conditions all together, it does NOT require insurers to provide coverage for their pre-existing condition – or prevent their premiums from being far more expensive.

I used to be a swing voter that leaned Republican. But, now that the Republican Party has reduced rare disease tax credits, is not protecting people with pre-existing conditions, and moved (in my opinion) far too quickly on a decision about a lifetime Supreme Court Justice who could determine the future of health care in this country... the GOP has single handedly forced me to move steadily and solidly to the left.

My family is a working, lower middle-class family, with a Federal health insurance plan. Between now and December we will work hard to pay all of our 2018 medical costs, because typically by February 1, 2019 we will owe $9,000 again.

We participate in grants and medication coupons to help us, but because of the new accumulators payors introduced this year (our insurance is one of them) which don’t count coupons and grants towards our deductible or out of pocket max, we’re likely going to owe even more next year. Meanwhile the insurance company will receive our deductible twice – once from our coupons and grants, then again from us directly.

This week I started selling our things on Facebook to help cover our medical bills, which is normal for many families dealing with expensive illnesses, but was somewhat shocking to many of my friends who reached out with offers of help and crowd-funding.

While the offers were sweet, we respectfully declined. Crowd-funding Jack’s medical needs is not sustainable. Unless health care in our country changes, these expenses will continue to build for the duration of Jack’s life. The single biggest thing you can do to truly help families like mine, is VOTE for candidates who will protect access to affordable health care for everyone who needs it.